State of your local property market: December 2023

By The Cooper Adams Team

Subscribe to newsletter

By The Cooper Adams Team

Subscribe to newsletterThere’s no denying that the last 12 months have had some people feeling like they’ve been on a 365 day long ride on the spinning tea cups. The UK property market has had its fair share of ups and downs and people’s confidence in the market has been about as robust as a pair of dissolving swimming trunks but there’s one thing that we can all agree on - the market is undoubtedly resilient.

The year 2023 has been marked by its extremes. The Bank of England's (BoE) fourteen consecutive interest rate hikes caused mortgage rates to soar, reaching their peak in August. The average rate for a two-year fixed and five-year fixed mortgage stood at 6.86% and 6.36%, respectively. Meanwhile, a decline in buyer demand caused house prices to experience their sharpest drop in fourteen years, with a significant slump occurring in October.

Despite the higher mortgage rates, the lower prices in the housing market balance it out. For instance, even if a mortgage costs an extra £20,000 over the long term, the house could be £35,000 less expensive, making you £15,000 better off, in theory. Moreover, there is a wider range of housing options available now, and you may be able to take advantage of sellers who are accepting lower offers. It's best to act now before the market returns to normal.

We want to reassure you that our local property markets, including Angmering, East Preston, Rustington, Worthing and Littlehampton all remain buoyant despite the economic changes. We appreciate our role and treasure our reputation in the community. Our reputation and unparalleled local knowledge distinguishes us from the rest. You can trust us when we say that the property markets are stable and prosperous. Don't let fear hold you back from making a change. We're here to help you break free from your current situation and find your new home.

Transactions are still taking place and supportive measures have been taken to encourage further activity in the industry. There’s even talk of cautious optimism rippling across the UK’s property market. Trust us to help you achieve your goals, we are as good as our word. Click here to find out what our customers think of us.

The current landscape

We have just stepped over the line of what historically marks the busiest week in online property searches; people step away from the Christmas dinner table and step up to the platform of online home searches, and deep dive into the new year market of property buyers and sellers. Estate agents are busy ensuring all listings are represented in the best possible light, communication channels are buzzing with activity, and sales progressors are exploding out of the starting blocks.

Contrary to media predictions, the UK's housing market has held up well in 2023 without crashing. While some house price indices suggest worrying trends, these are skewed towards borrowers who are affected by increased interest rates. The Office of National Statistics House Price Index indicates a more robust picture, showing only a 0.1% dip in house prices in the year to September.

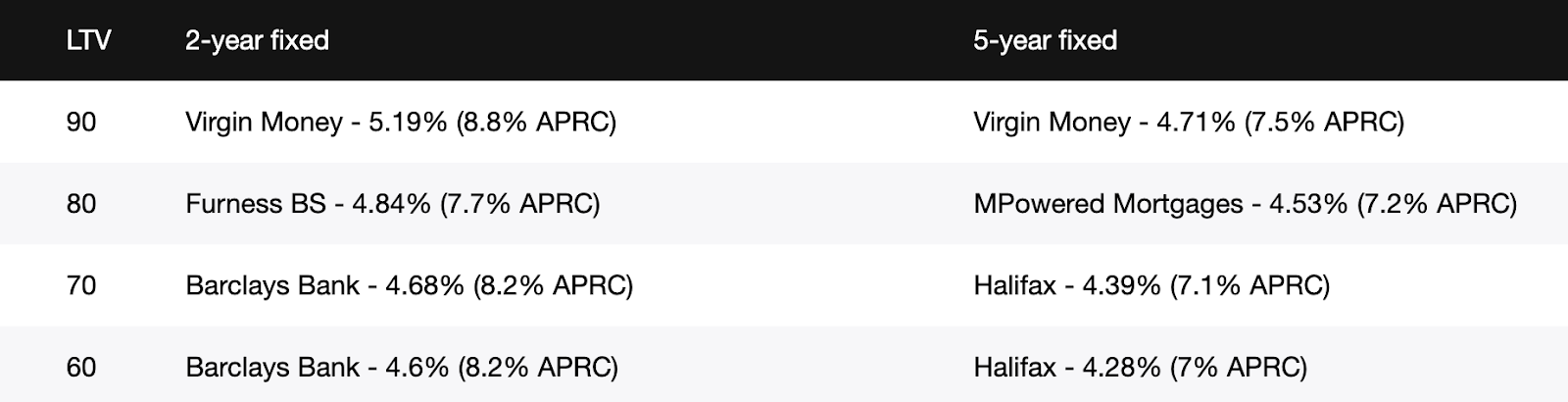

Mortgage rates

Compared to last year's tumultuous aftermath of former Prime Minister Liz Truss's disastrous Mini-Budget, the mortgage forecast for 2024 is much calmer. Fixed-rate mortgages have been decreasing for a few months due to better than anticipated inflation data and the general consensus that interest rates have reached their peak at 5.25%, following the Bank of England's decision to maintain the base rate for the second time in November 2023.

As of Friday 29th December 2023, the current average mortgage rates are shown below:

Rental market review

We caught up with Sam Dunnings, Head of Lettings at Cooper Adams to hear his take on the last 12 months:

“The rental market was extremely fast earlier in 2023, rents rising and lack of stock meant too many tenants fighting over available lets. With inflation rising the Bank of England increased interest rates to reduce spending and compress inflation. The lettings market did cool and towards the end of 2023 rents levelled out.

Tenants felt more confident that if they needed to move there was more choice for them so supply eased which in turn provided more competition and levelled rents.

Despite a record number of landlords leaving the market, citing high maintenance costs, tenant demand continues to rise in the private rental sector. This imbalance of supply and demand has resulted in bidding wars between tenants and a nationwide increase in rent. Consequently, government intervention has been prompted, with the Renters Reform Bill that was introduced in May, along with the recent announcement of the unfreezing of the local housing allowance (LHA) in last month's Autumn Statement.

Letting agents are now required to give more upfront information for tenants contemplating travelling distance to view which will add more transparency and a positive step”.

Shaun Adams, owner of Cooper Adams adds “We anticipate 2024 to remain level to start with, as mortgage rates are now dropping this will ease the burden on landlords with mortgages and decrease the pressure to raise rents”.

The road ahead

A lacklustre economy is being widely predicted for 2024, and that is likely to feed through to the housing market however we all know how the mainstream media likes to sensationalise disaster so don’t get swept up with the headlines without doing your own research and speaking to reputable sources.

Jeremy Leaf, the principal of a long-established North London estate agency and former RICS Residential Chair, says ‘We don’t expect to see much change in the next few months, rather a gradual improvement as optimism always seems to become more apparent at the beginning of the year.’

With that being said, the year 2024 is poised to be full of intrigue, with two landmark events on the horizon. Firstly, a General Election is expected to take place, during which housing issues will be a crucial topic of discussion (finally!). Secondly, the rental sector is expected to undergo significant changes, courtesy of new reforms that will likely be implemented before summer.

We understand that the current economic climate has made things difficult for many, with the rising rates and price movements. However, our branches have remained busy and experienced steady sales and lettings throughout 2023. With this in mind, we are confident that we can secure the best possible price for your property if you plan to let or sell in 2024.

"Property prices in the UK have surprisingly held up well over the past year, only decreasing by 1% annually to reach £283,615," says Kim Kinnaird, Director of Halifax Mortgages. However, this stability is more due to a scarcity of homes for sale than an increase in buyer demand. Despite the challenging market conditions, average house prices are only 3% lower than they were at their peak of £293,025 in August 2022, but still £44,000 higher than pre-pandemic levels. It's worth noting that the housing market has seen some fluctuations throughout 2023, which are somewhat masked by these figures."

In order to sell your property in a reasonable amount of time, it's best to align with our assessment of the local market value and set a price as close to it as possible. Hitting the market at a price above market value risks it taking longer to sell and therefore ‘going stale’. So much so, in fact, that a property that is put to market at the wrong level can cost you up to 11 extra weeks on the market. If you're not content with the local market value and opt for a higher price, you may have to wait longer to make a sale. Consider the financial and practical implications of waiting to sell your property before making this decision.