Capital gains tax

By Shaun Adams

Subscribe to newsletter

By Shaun Adams

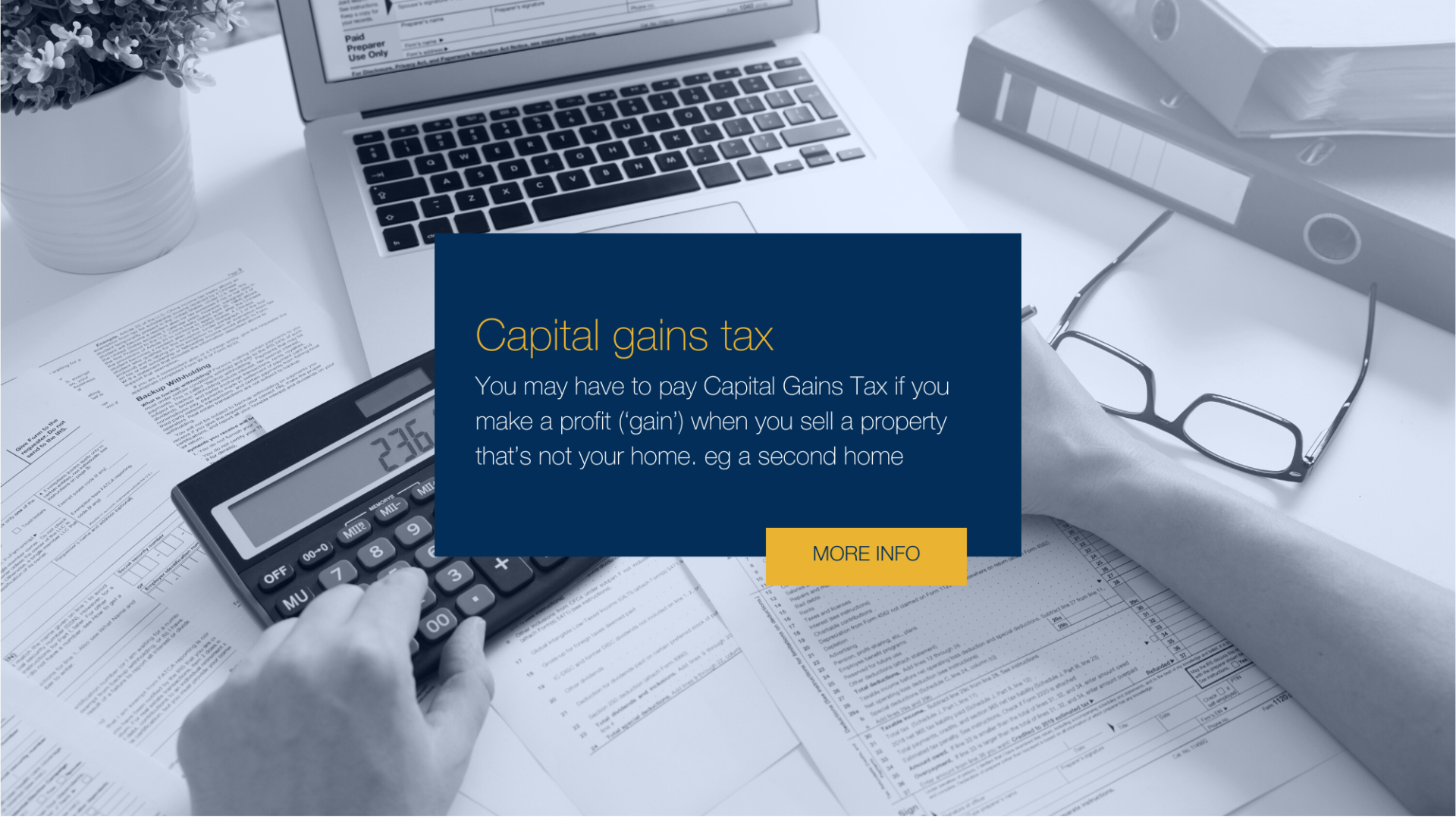

Subscribe to newsletterYou may have to pay Capital Gains Tax if you make a profit (‘gain’) when you sell a property that’s not your home. eg a second home

This could be a...

- buy-to-let properties

- business premises

- land

- inherited property

Here's how you work out your liability:

- Step 1 Start with the final value. This is usually the sale proceeds (or the market value if you give the item away).

- Step 2 Deduct the initial value. This is usually the price you paid or the market value when you were given the item. For anything you have owned since before 31 March 1982, it is the market value on that date.

- Step 3 Deduct any allowable expenses. These include the costs of buying and selling (for example, estate agents & solicitors costs, stamp duty, every single expense). They also include the cost of improving the asset (whatever you have spent on the property over the years), provided the improvement is reflected in the item's value.

- Step 4 If the answer is a loss, you can get tax relief by setting it against gains on other assets either this year or in future.

Now add together all your gains, deduct any losses and your annual tax-free allowance. For 2016-17 the allowance is £11,100, for 2015-16 it was £11,100.

So buying at £200,000 selling at £250,000 with £10,000 costs minus £22,000 allowance for a couple means you would pay CGT on £18,000 so either (£1,800 tax or £3,600)

For sales and gifts that you make in 2016-17, whatever remains is taxed at either 10% or 20% depending on your tax band (reduced from 2015-16 rates, which were 18% and 28% respectively).

Example capital gains tax calculation for 2016-17 Calculation Amount Capital gain £20,000 Losses £1,400 Annual allowance £11,100 Taxable gain = £20,000 – £1,400 – £11,100 £7,500 taxable gain CGT rate 10% tax rate Capital gains tax payable – £7,500 x 10% £750 payable

By

By

By

By